Financial happiness is not always just about accumulating as much as you can. Financial contentment can be achieved at all levels of wealth if you have a coherent plan that removes a lot of your anxieties about you and your family's future wellbeing. Here is a 10 steps route to putting in place a Financial Plan.

Step 1

Educate yourself

The journey to a good plan begins with education. Carry out your own research to educate yourself about financial matters. Understand and accept the gaps in your knowledge and take steps to fill these in. Learn about the happenings that will affect your financial future. Don’t be reluctant to talk to your financial adviser in order to enhance your knowledge.

Step 2

Set aside time to plan

It can take quite a while to review your finances and indeed this may need to involve other members of your family. It is well worth devoting the time, however, because it will give you a great starting point. Regular reviews, say once a year, are also needed.

Step 3

Assess your spending

Unfortunately not all of us have a good handle on how much we spend on a regular basis to the point where we don’t even know how much is left over in a typical weekly or monthly period. Knowledge is power in this respect. There are simple income and expenditure templates available to help. You will certainly find it useful in budgeting for large ticket items such as car and home insurance.

Step 4

Goal setting

In preparing your Financial Plan it is important to decide on your goals, be they short, medium or long term. A short term goal, for example, might be to buy a new car while a longer term goal may be to plan for retirement. Remember too that circumstances and priorities change over the years.

Step 5

Save regularly

Ad hoc savings just don’t work so the best advice is to have a regular savings project preferably through a standing order or direct debit. You should also plan to leave these savings alone for a considerable length of time in order to build up a good nest-egg. There are many savings plan options out there to help with this.

Step 6

Plan for your retirement

If you don’t have a Pension Plan of your own or you are not a member of an employer sponsored Plan then you should set one up sooner rather than later. A Pension Plan is unique in that you can avail of a tax benefit of up to 40% of anything you put in and also any investment growth is allowed to accumulate completely free of tax. If you have a Pension Plan make sure you know how much is in it and how it is invested. It is important to regularly review this to ensure you are setting aside enough for your future retirement needs.

Step 7

Review your tax returns

While there may not be many in number it is always worth checking that you are availing of all the tax allowances to which you are entitled. One such allowance is an annual capital gains tax allowance of €1270 which enables you to realise a gain on profits taken of this amount with no tax liability. There are other reliefs and incentives to be availed of also.

Step 8

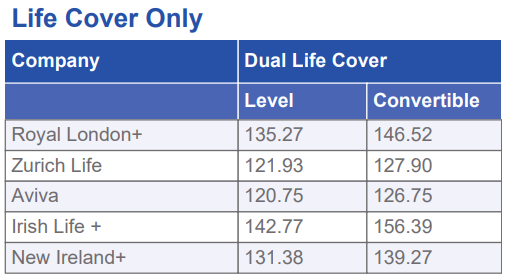

Life, Income Protection and Serious Illness Cover

If you can’t work or if you die prematurely what would happen to your family? If you are a business owner what happens if some catastrophe falls on you? This is where the need for Protection Insurance comes in bearing in mind that some of the required cover may already be in place.

Step 9

Have a Will and an Inheritance Plan

The first thing to say is that we should all have a valid will in place because in its absence you are only creating undue complications around where you would like your estate to go. Following on from this then is the question of Inheritance Tax and how this can be mitigated. One such mitigation, for example, is the utilisation of the annual gift tax allowance to pass lifetime assets from parent to child. Another consideration is that of the tax liabilities created for those who inherit substantial estates and how these can be planned for.

Step 10

Action Plan

While we can all have lots of good intentions about putting together a Financial Plan you can be certain of poor outcomes without proper follow through. Personal financial planning can often be as much about personal matters than financial. It is advisable therefore to use the services of a qualified and knowledgeable Financial Adviser to help with all that is involved. This is the area of our expertise so we would be very happy to hear from you.

When you have worked hard to create a reasonable nest egg the last thing you want is to see it lose value in real terms because you are holding it in cash deposits of one form or another. We are all too well aware of the fact that interest rates right now are at an all time low and even negative in some instances ------- the banks are actually charging you to hold on to your money!!

The longer you hold your money in cash the more value it will lose, particularly when inflation is taken into account.

"There's too much uncertainty right now" or "I'll put off investing for now until I see how things are going" are views we often come across. While it's completely natural to feel uncomfortable about moving to active investments, you are after all transitioning from a position of comfort to one that involves risk, there are many options available that help to mitigate the risk involved.

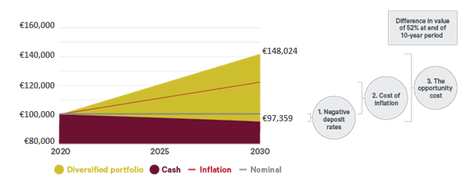

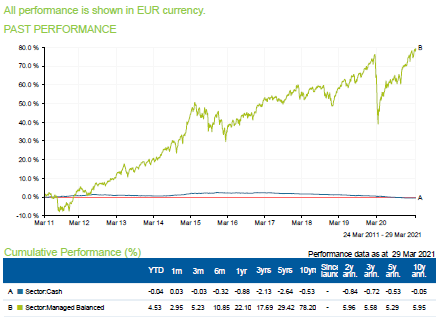

Keeping money on deposit comes at a cost. In essence that cost is no growth. Take a look at the illustration below:

When you have worked hard to create a reasonable nest egg the last thing you want is to see it lose value in real terms because you are holding it in cash deposits of one form or another. We are all too well aware of the fact that interest rates right now are at an all time low and even negative in some instances ------- the banks are actually charging you to hold on to your money!!

The longer you hold your money in cash the more value it will lose, particularly when inflation is taken into account.

"There's too much uncertainty right now" or "I'll put off investing for now until I see how things are going" are views we often come across. While it's completely natural to feel uncomfortable about moving to active investments, you are after all transitioning from a position of comfort to one that involves risk, there are many options available that help to mitigate the risk involved.

Keeping money on deposit comes at a cost. In essence that cost is no growth. Take a look at the illustration below: